Work Opportunity Tax Credit

IRS

Guide

Last updated:

November 4, 2025

The Work Opportunity Tax Credit (WOTC) is a federal tax credit offered by the IRS to incentivize employers to hire individuals from specific targeted groups facing barriers to employment. It’s a win-win: employers gain valuable team members, while at-risk employees find opportunities to enter the workforce.

This program also aligns with workforce initiatives to promote workplace diversity and expand job opportunities for American workers.

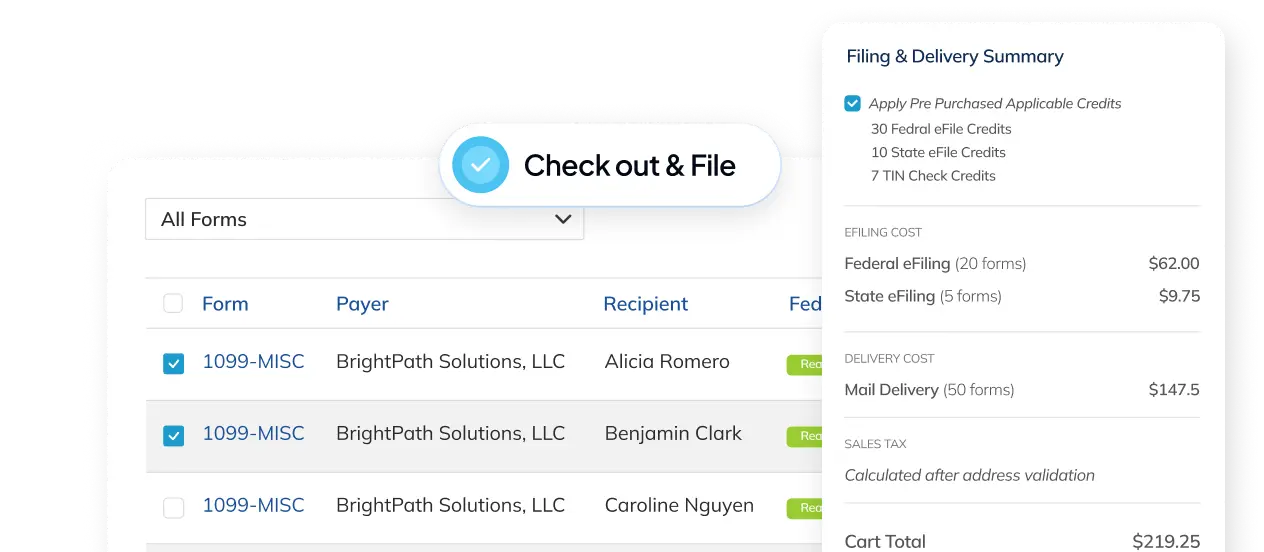

{{rich-card}}

The WOTC is calculated as 40% of up to $6,000 in wages paid to an employee who:

The maximum tax credit is typically $2,400 per eligible employee, making this a great way for employers to reduce tax liability while supporting workforce diversity.

The IRS and the Department of Labor jointly administer the WOTC. Employers must request certification by filing IRS Form 8850 and submitting it to the appropriate state workforce agency within 28 days of the employee’s start date.

{{CTA}}

Employers can claim the WOTC when they hire individuals certified as members of targeted groups. These groups include, but are not limited to:

Visit the IRS website for a full list of qualifying groups.

Save up to 45 days by skipping the wait for IRS processing.

Save up to 45 days by skipping the wait for IRS processing.

Save up to 45 days by skipping the wait for IRS processing.

Social Security Administration Direct Operations CenterWilkes-Barre, PA 18769-0001 (for Certified Mail Use ZIP code 18769-0002)

Social Security Administration Direct Operations CenterP.O. Box 3333 Wilkes-Barre, PA 18767-3333.

Reduce the 250-return threshold enacted in prior regulations to generally require electronic filing by filers of 10 or more returns in a calendar year. The final regulations also create several new regulations to require e-filing of certain returns and other documents not previously required to be e-filed.

Require filers to aggregate almost all information return types covered by the regulation to determine whether a filer meets the 10-return threshold and is required to e-file their information returns. Earlier regulations applied the 250-return threshold separately to each type of information return covered by the regulations.

Eliminate the e-filing exception for income tax returns of corporations that report total assets under $10 million at the end of their taxable year, and require partnerships with more than 100 partners to e-file information returns, and they require partnerships required to file at least 10 returns of any type during the calendar year to e-file their partnership return.

Corrections must be filed the same way the original was submitted. If you eFile the original then you must eFile the correction. If you mailed in the original then you must mail in the correction.

Do not cut or separate Copies A of the forms that are printed two or three to a sheet, except for Form W-2G. Generally, Forms 1097, 1098, 1099, 3921, 3922, and 5498 are printed two or three to an 8" x 11"sheet. Form 1096 is printed one to an 8" x 11" sheet.

These forms must be submitted to the IRS on the 8" x 11" sheet. If at least one form on the page is completed, you must submit the entire page. Forms W-2G are an exception and may be separated and submitted as single forms. Send your forms to the IRS in a flat mailing (not folded).

Do not staple, tear, or tape any of these forms. It will interfere with the IRS’s ability to scan the documents.

Pinfeed holes on the form are not acceptable. Pinfeed strips outside the 8" x 11" area must be removed before submission without tearing or ripping the form. Substitute forms prepared on continuous feed or strip form paper must be burst and stripped to conform to the size specified for a single sheet (8" x 11") before they are filed with the IRS.

Do not use a form to report information that is not properly reportable on that form. If you are unsure of where to report the data, call the information reporting customer service site at 1-866-455-7438 (toll free).

Do not submit anything other than red ink copies to the IRS.

Use the official forms or substitute forms that meet the specifications in Pub. 1179. If you submit substitute forms that do not meet the current specifications and that are not scannable, you may be subject to a penalty for each return for improper format. All of Adam’s tax forms meet the proper requirements, so use us as a resource.

Do not use dollar signs ($) (they are pre-printed on the forms), ampersands (&), asterisks (*), commas (,), or other special characters in money amount boxes.

Do not use apostrophes (’), asterisks (*), or other special characters on the payee name line.

No photocopies of any form are acceptable.

Do not print plain ink copies of your W-2 copy A or W-3 form. If a box doesn't apply to you, leave it empty.

Do not add "0".

Do not omit the decimal point and cents from entries.

Do not mistakenly check the “Retirement plan” checkbox in box 13. See page 22 of this IRS PDF for Retirement plan details.

Do not misformat the employee’s name in box e. Enter the employee’s first name and middle initial in the first box; his or her surname in the second box; and his or her suffix (such as “Jr.”) in the third box (optional).

Do not enter the incorrect employer identification number (EIN) or the employee’s SSN for the EIN.

Do not cut, fold or staple Copy A paper forms mailed to SSA.

Do not mail any copy other than Copy A of Form W2 to the SSA.

File the correct form with the correct amount, code, checkbox, name or address, and check the “CORRECTED” box. This overwrites what you originally filed with the IRS under that person or company’s name and TIN. Send the corrected form to the recipient and prepare the red Copy A to send to the IRS with the Form 1096 transmittal if you’re paper filing. If you also had the wrong recipient/payee name or TIN do a Type 2 correction instead.

For Type 2 errors, either the recipient/payee name and/or the TIN are wrong or you used the wrong form (like a 1099-MISC instead of a 1099-NEC). Action: This is a two-step process. First, you must zero out what you filed with the IRS under the wrong name/TIN and then file the new form.

Step 1

File a form with the CORRECTED box checked and the exact same payer and recipient information as on the incorrect form, but with all the amounts as zeros. This will remove the originally filed form from the IRS records.

Step 2

File a new Form 1099 with the right information as an originally filed form (not a corrected form).

Incorrect Payer Name, Payer TIN, or both Action: Write a letter to the IRS.

If you filed with the wrong payer name (yours or your client’s name/company name) or the wrong payer taxpayer identification number (TIN), you don’t need to send in a corrected form.

Instead, you should write a letter containing the following information:

Name and address of the payer

Type of error (including the incorrect payer name/TIN that was reported)

Tax year Payer TIN Transmitter Control Code (if you eFiled),

Type of return, Number of payees, Filing method (paper or eFiling)

You have exceeded the IRS paper filing threshold and are required to file electronically.